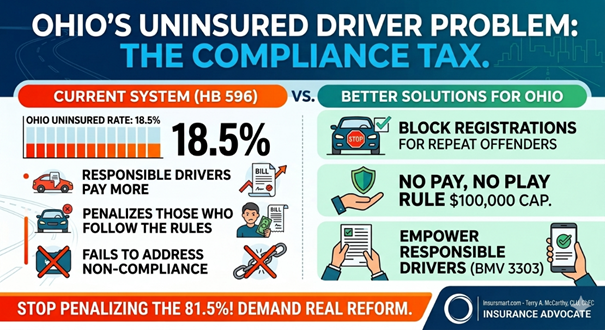

Nearly 1 in 5 drivers on Ohio roads has no insurance—18.5% according to the latest 2025 Insurance Research Council data. While House Bill 596 is marketed as a “safety net,” a technical analysis reveals it to be a “compliance tax” that penalizes the responsible to subsidize the lawless. It is a lazy effort that refuses to confront the root of the problem.

The Conflict of Interest: Why I Am Opposing This Bill

As an agency owner, the logic of HB 596 would technically benefit my bottom line: doubling mandates and forcing coverage leads to higher premiums and higher commissions. However, as a CLU® and ChFC®, my fiduciary-level training compels me to speak out. This bill is a bad deal for Ohio families, a professional liability minefield for agents, and a gift to those who refuse to follow the law.

The Failure of HB 596: Subsidizing Non-Compliance

- The Price-Out Effect: By forcing higher limits, the state makes legal insurance less affordable for the “working poor,” likely pushing the uninsured rate even higher. I am not against higher limits. I am against foisting the uninsured dilemma on the compliant.

- The Agent’s E&O Minefield: HB 596 creates a massive Errors & Omissions (E&O) risk for agents. By doubling minimum limits and mandating specific coverages, the state creates a new “duty to advise.” Agents become the face of a state-mandated price hike, risking professional negligence claims during the transition. We are being forced to act as uncompensated state administrators while our professional liability increases.

- The Economic Transfer: Responsible Ohioans already bear a $400+ million annual burden in higher premiums, lost wages, and unrecoverable medical debt. HB 596 doesn’t stop this drain; it formalizes it.

- The Monitoring Illusion: Some propose solving the problem through expanded centralized electronic monitoring. This adds another layer of government scrutiny on the 81.5% who already obey the law but delivers no meaningful reduction in the uninsured rate. It simply creates more administrative burden and privacy concerns for responsible policyholders.

The Professional Alternative: Front-End Accountability

We must stop the 18.5% at the point of entry. Ohio has the digital infrastructure to do this now; we simply lack the legislative will.

The “Dealer Gatekeeper” & Registration Barrier

We must close the Dealer Loophole:

- The “Naughty List” Integration: Dealers and BMV registrars must have real-time electronic access to a “proven uninsured” database. If a buyer has a recent violation or suspension for driving without insurance, the system must automatically block registration.

- 3-Year SR-22 Mandate: This block remains in place until the individual proves 1–3 years of continuous, verified coverage (SR-22). You cannot get a plate until you prove you are part of the system.

Felony Aiding & Abetting: Putting Enablers on the Hook

We must make those who facilitate lawlessness legally culpable:

- The Interlock & Loaner Felony: If a family member blows into an ignition interlock or knowingly loans a vehicle to an uninsured driver, they are committing a felony.

- The Fear of Outcome: When the “inner circle” understands that enabling an uninsured driver carries life-altering criminal risk, the offender loses the mobility that allows them to remain outside the law.

The Expanded Louisiana “Hammer” ($100k Statutory Bar)

We must remove the “Free Rider” profit motive. I am advocating for an aggressive evolution of the Louisiana model (R.S. 32:866). An uninsured driver should be barred from recovering the first $100,000 in bodily injury and $100,000 in property damage—even if they are not at fault. By establishing this high statutory deductible, we force the lawless to internalize the true cost of their choice. If you don’t contribute to the pool, you don’t collect from it.

Citizen-Led Enforcement (BMV 3303)

We must educate the public on the power they already have. If you are hit by an uninsured driver, you can trigger their license suspension today by submitting Form BMV 3303. To ensure accountability:

- Filing: You can file if the accident was in Ohio, the driver was uninsured, and damage exceeds $400 (property) or $500 (injury).

- The Three-Identifier Rule: You must provide three matching identifiers (Name, Address, DOB, License #, or SSN) to the BMV within six months.

- Result: The offender’s license stays suspended until they pay your damages in full or post a cash deposit with the state.

Conclusion: 18.5% is Proof of a Failed Status Quo

An 18.5% uninsured rate—ranking Ohio 12th worst in the nation—is evidence that our current enforcement is a paper tiger. HB 596 is a lazy effort that passes the bill to the 81.5% of Ohioans doing the right thing. We do not need more intrusion on the compliant; we need to make being uninsured—and helping the uninsured—statutorily and criminally ruinous. Let’s stop taxing the responsible and start holding the lawless and their enablers accountable.

About the Author:

Terry A. McCarthy, CLU, ChFC, AMTC Graduate, was an authorized Ohio instructor for insurance pre-licensing and continuing education, and a graduate of Central Michigan University. An elite-credentialed agent specializing in complex risk assessment, his agency focuses on tailored solutions for families, artisan contractors, businesses and medical and dental practices.

Agency: Insurance Associates Agency Inc.

Website: insursmart.com

Sources: Insurance Research Council (IRC) 2025 Study; Ohio Insurance Agents Association; Louisiana R.S. 32:866; Ohio BMV.